Tim Baker, CFA

Founder & CEO

The Factor Report

Week Ended July 31, 2026

Market Wrap

For the week ended July 31st, 2026, stocks were higher everywhere. Bonds were lower for the week as the iShares Core US Aggregate Bond ETF (AGG) fell 0.75% with yields rising; the 10-year US treasury yield increased to 4.74%, according to Yahoo Finance. Asset price drivers of the week:

- Monday started with a bang and ended with a fizzle, at least in the US. Another ceasefire with Iran kicked things off on a positive note, but fears about Tech profitability quelled the enthusiasm.

- Strong earnings from Visa and Coca Cola fueled a bit of a rally on Tuesday.

- Wednesday was a difficult day for investors. Oil jumped over 6% as fighting continued in Iran. Federal Reserve Chairman Kevin Warsh announced the central bank was keeping rates on hold, but indicated there would be a hike later in the year if inflation remains unchecked.

- Thursday brought a sharp rebound after Microsoft's strong earnings report Wednesday evening and the Fed's preferred measure of inflation fell slightly for the month of June.

- Stocks continued the rally on Friday as investors were reinvigorated about the "AI trade", especially after Amazon's stellar earnings.

- Next week we will get a number of key data points on the health of the manufacturing sector, as well as a couple of important employment reports including the July jobs report on Friday.

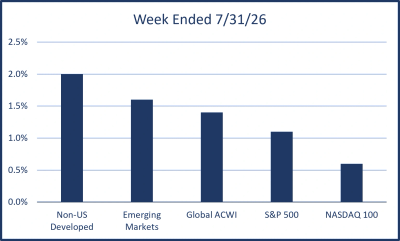

Performance Summary

As shown in the chart, Non-US Developed again held up the best for the week. Emerging Markets also beat the global index while the US lagged. Within the US, the tech-heavy Nasdaq was by far the biggest drag on the broader market as the more traditional stocks of the Dow Jones Industrial Average outperformed. From a factor perspective, Quality in the US beat the broader S&P 500.

In The News

A new retirement plan idea from the person that invented the 401(k).

Flows to bond funds may be good for stocks.

Why one strategist thinks the resilience of stocks means it's time to go all-in.

Disclosures

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy will be profitable or equal the corresponding indicated performance level(s). Moreover, you should not assume that any of the above content serves as the receipt of, or as a substitute for, personalized investment advice from Metric Financial.

All data and performance information sourced from Morningstar and MarketWatch, unless otherwise indicated.

USA is the MSCI USA index, Non-US Developed is the MSCI EAFE index, Emerging Markets is the MSCI Emerging Markets index, and All Country World is the MSCI ACWI index. One cannot invest in an index. Because the factor indexes have varying inception dates, some of the returns provided are back-tested and do not represent actual performance. Inception dates are as follows:

Momentum = MSCI ACWI Momentum NR USD Index (Inception: 11/30/95)

Value = MSCI ACWI Enhanced Value NR USD Index (Inception: 5/29/15)

Quality = MSCI ACWI Quality NR USD Index (Inception: 5/29/92)

Low Volatility = MSCI ACWI Minimum Volatility (USD) NR USD Index (Inception: 5/28/93)

Size = MSCI ACWI Risk Weighted NR USD Index (Inception: 4/6/11)

Metric Financial, LLC (“Metric”) is a registered investment adviser offering advisory services in the State of Connecticut and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. Follow-up or individualized responses to consumers in a particular state by Metric in the rendering of personalized investment advice for compensation shall not be made without our first complying with jurisdiction requirements or pursuant to an applicable state exemption.

All written content is for information purposes only. Opinions expressed herein are solely those of Metric, unless otherwise specifically cited. Material presented is believed to be from reliable sources and no representations are made by our firm as to another parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation.

Returns for ETFs representing the designated geographies. Source: investing.com